If you are administering a private company stock option plan, you need to do what is referred to as “the Rule 701 math” before every grant of stock options or equity awards.

What is “the Rule 701 math”?

Rule 701 contains a set of mathematical limitations on how many shares of stock you can offer service providers during any consecutive 12-month period. If you exceed Rule 701’s mathematical limits, you might not have a securities law exemption for the equity you award in excess of the limit (you couldn’t rely on Rule 701, but perhaps there are other exemptions you could find).

If you blew Rule 701 and issued securities without a securities law exemption, this would be a serious issue for your company. You don’t want to do this for all sorts of reasons. One reason is that it might cause the delay of your company’s public offering (this actually happened to Google).

The Mathematical Limitations

There are three mathematical measures under Rule 701. You get to choose the greatest of the 3 measures. The three measures apply during any consecutive 12-month period. The three measures are:

- $1M;

- 15% of balance sheet assets; or

- “15% of the outstanding amount of the class of securities being offered and sold in reliance on this section.”

The $1M test is the easiest to apply because you don’t have to refer to the company’s balance sheet or cap table. If you are a startup, and you are granting stock options at $1.00 a share, then during any consecutive 12-month period you can’t grant options on more than 1M shares.

So, the $1M test is especially helpful to early stage companies, whose common stock price per share might be low.

But as your price per share increases, you might find yourself having to rely on one of the 15% tests.

In particular, you might want to know–how do you determine 15% of the outstanding amount “of the class of securities being offered and sold in reliance on this section”? And what is meant by “class of securities being offered”?

If you are like most companies, your founders own common stock, and your option pool is common stock, but you have issued your investors convertible preferred stock.

If you keep reading Rule 701, you will find a rule explaining how you go about “calculating prices and amounts.”

In particular, Rule 701(d)(3)(iii) says as following:

In calculating outstanding securities for purposes of paragraph (d)(2)(iii) of this section, treat the securities underlying all currently exercisable or convertible options, warrants, rights or other securities, other than those issued under this exemption, as outstanding.

The above language is helpful.

Let’s suppose your company has a typical cap structure. The Founders own 4M shares, there is an option pool of 1M shares, and your Series Seed Preferred investors own 1.5M shares of Series Seed Preferred. Your cap table thus looks as follows:

|

|

|

| Common |

4,000,000 |

61.54% |

| Pool |

1,000,000 |

15.38% |

| Series Seed Preferred |

1,500,000 |

23.08% |

|

6,500,000 |

|

Say you want to rely on the 15% of the outstanding class of securities being offering test. How do you determine the 15%? Is it 15% of the Founder Common Stock? Or is it 15% of the Founder Common Stock AND the Series Seed Preferred.

Well, if you read the rule on how to calculate prices and amounts it told you:

Rule 701(d)(3)(iii): In calculating outstanding securities for purposes of paragraph (d)(2)(iii) of this section, treat the securities underlying all currently exercisable or convertible options, warrants, rights or other securities, other than those issued under this exemption, as outstanding.

This is helpful. The Series Seed is convertible to common by the holders at any time, and the Series Seed wasn’t issued under Rule 701 but Rule 506. So, it would make sense to include the preferred as well as the common in doing your math.

But what about the “class” of securities being offered component of the test? The “rules for calculating prices and amounts” don’t say anything about the “class” question. In fact, the only place the word “class” appears in Rule 701 at all is in the 15% of outstanding securities rule. There is no other mention of class.

There is an SEC no-action letter on the “class” issue. But what is odd about the Arclight no-action letter is there is no reference in it to Rule 701(d)(3)(iii). As the letter requesting the no-action letter says:

Rule 701 does not contain a definition of “class” of securities for the purpose of determining whether the A, B and C Units should be considered a single “class” of securities in calculating the amount of offers and sales Arclight may make under Rule 701.

Perhaps the lawyers writing the Arclight letter simply didn’t think Rule 701(d)(3)(iii) relevant because it says nothing about “class.”

Perhaps the word “class” is not to be given any special significance? This is probably too hopeful of an interpretation.

In trying to understand this issue a little more, I found this series of letter exchanges between the SEC and a company trying to go public helpful and informative.

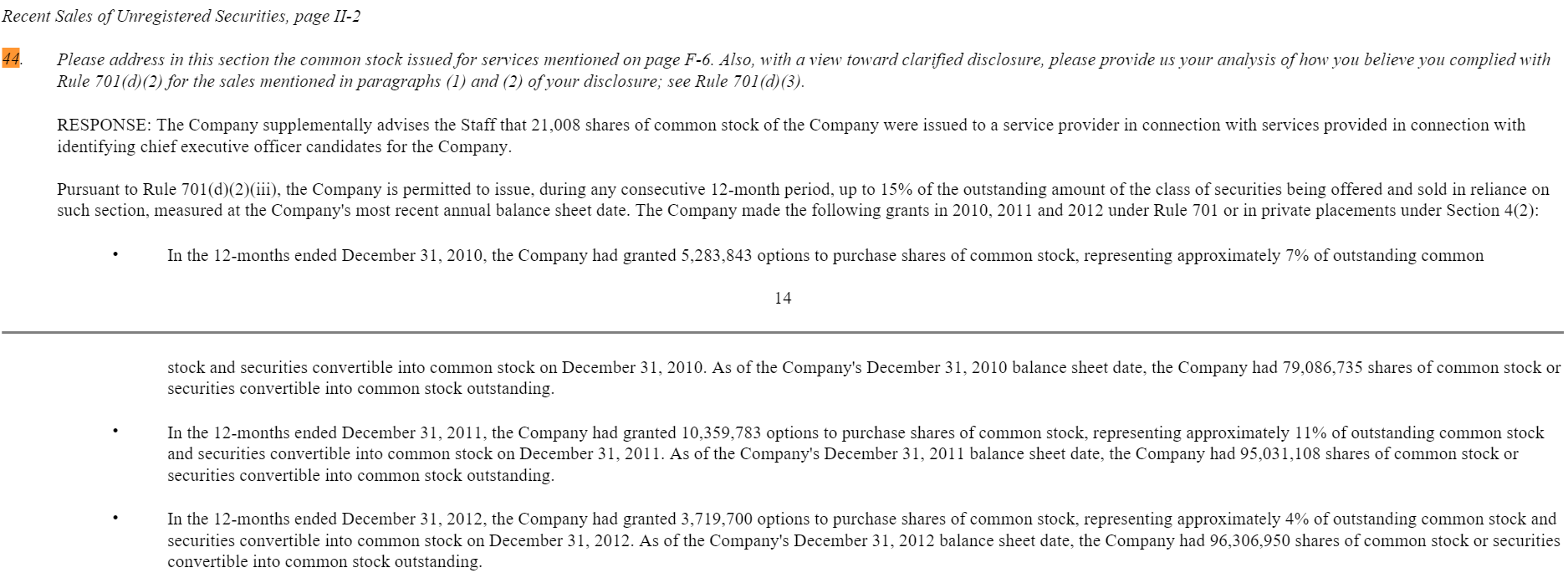

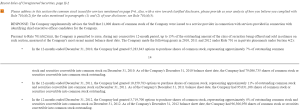

Here is what happened:

The company filed a draft registration statement with the SEC. In the draft registration statement, the company’s statement of stockholders’ equity showed the issuance of common stock in exchange for services.

The SEC asked about this in its comment letter.

The Company submitted another draft registration statement, and a reply to the SEC’s letter.

In its response letter, the company said the following:

But the SEC still wasn’t satisfied, and asked in its next letter, a little more pointedly, the following question:

Please expand your response to prior 44 to provide us your analysis of the applicability of the authority on which you rely to conclude that you may consider “securities convertible into common stock” as part of the number of shares of “outstanding” common stock for purposes of Rule 701(d)(2)(iii).

In its response, company simply quotes Rule 701(d)(3)(iii), and rests its case.

19. Please expand your response to prior 44 to provide us your analysis of the applicability of the authority on which you rely to conclude that you may consider “securities convertible into common stock” as part of the number of shares of “outstanding” common stock for purposes of Rule 701(d)(2)(iii).

RESPONSE: The Company respectfully advises the Staff that Rule 701(d)(3)(iii) provides as follows:

“In calculating outstanding securities for purposes of paragraph (d)(2)(iii) of this section, treat the securities underlying all currently exercisable or convertible options, warrants, rights or other securities, other than those issued under this exemption, as outstanding.”

As such, the Company included outstanding common stock, outstanding convertible preferred stock and outstanding warrants to purchase shares of convertible preferred stock and common stock not issued pursuant to Rule 701 as part of the number of shares of outstanding common stock for purposes of Rule 701(d)(2)(iii).

It would be nice if the SEC issued a telephone interpretation putting any potential lingering questions here definitively to bed.