The difference between an ISO and an NSO can change the after-tax value of a single option grant by tens of thousands of dollars — and the decisions that determine which treatment you get are made at grant and exercise, long before any money changes hands. Most people learn the distinction only after it has cost them. This guide to equity compensation's most consequential fork covers the rules before they cost you.

For NSOs specifically, employers must also handle tax withholding on NSO exercises.

In This Guide

- → What ISOs and NSOs Actually Are

- → The Tax Difference: Why Timing Changes Everything

- → The Alternative Minimum Tax Trap

- → The $100,000 ISO Annual Vesting Limit

- → Who Can Receive ISOs and NSOs

- → Capital Gains and the Qualifying Disposition Test

- → The Three-Month Post-Termination Exercise Window

- → Section 83(b) Elections and Early Exercise

- → QSBS and Both ISO and NSO Implications

- → Washington State Income Tax: How ESSB 6346 Changes the Calculus

- → When Founders Should Grant ISOs Versus NSOs

- → The Company Tax Deduction: An Often-Overlooked Advantage of NSOs

- → Common Mistakes and How to Avoid Them

- → Strategic Considerations for Growing Companies

- → The Bottom Line

- → Ready to Build on a Solid Legal Foundation?

Stock options seem simple on the surface. Your company grants you some options. You exercise them at some point. You sell the stock. You pay taxes. Done, right?

Wrong. The actual mechanics, the timing, the rules about who gets what kind of option, and the interaction with half a dozen other tax rules? That's where the complexity lives. And that's where founders and employees leave money on the table.

This guide covers everything you need to know about ISOs and NSOs: what they are, when a company should grant one versus the other, what the real tax consequences look like, and how to avoid the mistakes that cost people—and companies—real money.

What ISOs and NSOs Actually Are

Let's start with the fundamentals. A stock option is simply a contractual right to purchase shares of your company at a predetermined price—what we call the strike price or exercise price. You don't own the stock yet. You own the right to buy the stock at that fixed price, whenever you decide to exercise that right (within the terms of your grant).

That's where ISOs and NSOs are the same. That's also where the similarities end.

An ISO—Incentive Stock Option—is a creature of federal tax law, specifically IRC Section 422. Congress created ISOs in 1981 as a way to align employee interests with company performance while providing favorable tax treatment. When you exercise an ISO, you don't immediately owe ordinary income tax on the difference between what you paid for the stock and what it's worth. That's the magic of an ISO, and we'll dig into why that matters in a moment.

An NSO—Nonqualified Stock Option—is everything else. It's not qualified for the special ISO treatment. When you exercise an NSO, the difference between the strike price and the fair market value of the stock at exercise is treated as ordinary income. You pay federal income tax, payroll taxes (FICA withholding if you're an employee; self-employment tax if you're a contractor), state income tax, and everything else that applies to compensation income.

The naming is a bit unfortunate because "nonqualified" makes NSOs sound like second-class options. In reality, NSOs are incredibly useful and often the right choice for a company. More on that in a moment.

But first, why this distinction matters so much in the real world.

The Tax Difference: Why Timing Changes Everything

Imagine I grant you 10,000 shares as an NSO with a $1.00 strike price. You hold the option and exercise later, once the stock's fair market value has climbed to $1.50 per share. You pay $10,000 (10,000 shares × $1.00 strike price). But the stock is worth $15,000 on the day you exercise ($1.50 × 10,000 shares).

That $5,000 difference—the "spread" between the strike price and the fair market value—is ordinary income. Right now, on that day, you owe federal income tax, Social Security and Medicare taxes, and state income tax on that $5,000. Even though you haven't sold a single share. Even though the stock might go to zero. You owe the tax regardless.

Now imagine the same scenario with an ISO. Same grant, same strike price, same fair market value at exercise. You exercise the 10,000 shares. You pay $10,000. But here's the difference: you don't owe ordinary income tax on that $5,000 spread at exercise. Nothing. Zero federal income tax. No state income tax (in most cases). No employment taxes.

That's the core benefit of an ISO, and it's substantial.

But here's where people often misunderstand it: you don't get away from capital gains tax. If you hold the stock for the right amount of time and satisfy certain conditions—which we'll discuss—you'll eventually sell the stock. When you do, you'll owe capital gains tax on the entire gain from your original $1 strike price to whatever you sell it for. But capital gains rates are lower than ordinary income rates, and you get to defer the tax until you actually sell.

With an NSO, you owe ordinary income tax immediately on the spread, and then capital gains tax on any further gain when you sell. That's two tax hits, and the first one can be brutal because you owe it before you've actually made any money.

The Alternative Minimum Tax Trap

Now I need to tell you about something that very few startup employees understand until it's too late: the Alternative Minimum Tax, or AMT.

The AMT is a parallel tax system that exists to prevent high-income people from using certain deductions and exclusions to avoid federal income tax entirely. For most people, the AMT doesn't apply. But for ISO holders, it can be devastating.

Here's why: when you exercise an ISO, there's no ordinary income tax. But the exercise creates an "alternative minimum taxable income" adjustment equal to the spread. So even though you didn't owe regular federal income tax on the spread, the spread counts toward your AMT calculation.

If your AMT ends up being higher than your regular federal income tax, you pay the AMT instead.

This might sound abstract, so here's a concrete example. Suppose you exercise 100,000 ISO shares at $1 per share when the stock is worth $10 per share. That's a $900,000 spread. No ordinary income tax due, but you now have a $900,000 AMT adjustment. If you have significant other income, this could easily push you into AMT territory. When it does, you might owe $200,000, $300,000, or even more in AMT that you otherwise wouldn't have owed.

The cruel part? You can take a credit for AMT paid in future years, but the credit can only offset regular tax, and it phases in slowly. If you pay a massive AMT bill in year one and then your company never goes public, you might never recover that credit.

This is not theoretical. During the dot-com boom, thousands of employees exercised ISOs in companies that eventually failed or stayed private for decades. They owed AMT on the spread immediately but never made any money from the stock. Some of them are still fighting with the IRS over this nearly 25 years later.

This is the reason many sophisticated employees, when they understand the math, actually prefer NSOs. You owe tax immediately, but at least you know your liability. You pay it, move on, and you're protected if the stock never goes anywhere.

The $100,000 ISO Annual Vesting Limit

Here's another rule that trips up founders: Section 422(d) of the IRC limits the number of ISO shares that can vest in a single calendar year.

Specifically, the aggregate fair market value of the stock with respect to which ISOs are exercisable for the first time in any calendar year (determined at the time of grant) cannot exceed $100,000. The “for the first time” language matters: the limit applies to shares as they first become exercisable each year, not to your cumulative exercisable balance.

What does "exercisable" mean? Generally, shares that have vested and become exercisable under the option agreement. So if you grant someone 40,000 ISOs with a four-year vest and one-year cliff, then 10,000 shares vest each year. In year one, 10,000 shares are exercisable (fair market value of $100,000 or less). In year two, another 10,000 shares vest and become exercisable. And so on.

But here's the practical implication: if the strike price is very low relative to fair market value, you can hit this $100,000 limit with a relatively small number of shares. Because the limit is measured by the fair market value at grant, a higher valuation means fewer shares fit under it. If the fair market value at grant is $1 per share, only 100,000 shares can become first exercisable per year as ISOs before hitting the limit. If the stock is worth $5 per share at grant, only 20,000 shares per year can qualify.

Anything over this limit automatically becomes an NSO, regardless of what your option agreement says.

This is relevant for companies that have had multiple funding rounds. Early employees might be granted options with low strike prices and small fair market values. Later employees might be granted options at much higher strike prices, because the company is worth more. But it still applies. If the aggregate of all ISOs you've granted to an employee crosses $100,000 in fair market value per year, the excess becomes NSOs.

For this reason, many sophisticated companies grant only NSOs to employees after the first round or two of funding, simply to avoid this complexity. As the company's valuation rises, the ISO limit becomes harder to stay within.

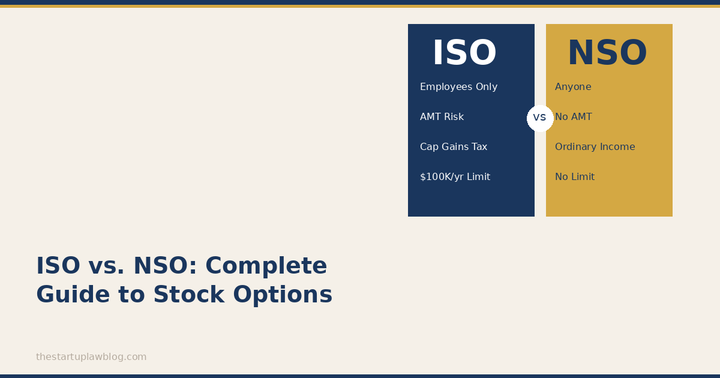

Who Can Receive ISOs and NSOs

This is a straightforward rule, but it matters: ISOs can only be granted to employees. That's it. Not consultants. Not board members. Not advisors. Only employees.

The IRS is strict about this. If you grant an ISO to a consultant or contractor, it loses its ISO status and becomes an NSO, regardless of what the agreement says.

NSOs, on the other hand, can be granted to anyone: employees, consultants, advisors, board members, investors, even family members if you want (though that raises other issues). This is one of the big reasons NSOs are so common in startup equity packages.

If you want to give your early advisors equity incentives, you're granting NSOs. If you want to give your board members options, NSOs. If you want to pay a consultant partly in options, NSOs. ISOs are exclusively for the employees you're trying to incentivize to stay and perform.

Capital Gains and the Qualifying Disposition Test

Remember when I said ISOs have special tax treatment? I didn't tell you the full story. There are conditions.

To get the benefit of the ISO—to avoid ordinary income tax on the spread at exercise—you have to satisfy what the tax code calls a "qualifying disposition." It's not complicated, but it is mandatory.

A qualifying disposition means: (1) you hold the stock for at least two years from the date the option was granted, and (2) you hold the stock for at least one year from the date you exercised the option.

If you meet both of these conditions, the entire gain—from strike price to sale price—is treated as long-term capital gain. You pay capital gains tax, not ordinary income tax. Much better.

If you don't meet these conditions, it's called a "disqualifying disposition." And here's what happens: the spread between the strike price and the fair market value on the date of exercise is taxed as ordinary income, just as if you'd exercised an NSO in the first place. Any additional gain after the exercise date is still capital gain. But you've lost the ISO benefit on the spread. One relief rule worth knowing (§422(c)(2)): if you sell in an arm's-length disqualifying disposition for less than the exercise-date fair market value, your ordinary income is generally limited to your actual gain on the sale — you aren't taxed on paper spread you never realized. In a down market, that cap matters.

The most common reason for a disqualifying disposition? You leave the company, exercise the options, and sell the stock all within a year. You exercised the option and held the stock for less than one year, so the disposition doesn't qualify.

This is important enough that I'm going to say it again: if you exercise an ISO, you need to hold the stock for at least one year before selling to avoid ordinary income tax on the spread. Some employees don't realize this. They exercise their options, their company has a successful exit, and they're suddenly forced to pay ordinary income tax instead of capital gains tax because they didn't hold long enough.

The Three-Month Post-Termination Exercise Window

Most stock option plans, whether they're for ISOs or NSOs, include a vesting schedule. Typically, 25% of your shares vest after one year (the "cliff"), and the remaining 75% vest monthly or quarterly over the next three years. If you leave the company, you can only exercise the shares that have vested.

But here's where ISOs have a special rule: if you leave the company, you have only three months to exercise your vested ISOs and keep ISO tax treatment (§422(a)(2)). Two different things can happen at the three-month mark, and it pays to know which applies to you. Under most standard plans, the option simply expires — the plan is written to terminate options at three months precisely because ISO treatment ends there. But the three-month cutoff itself is a tax rule, not an expiration rule: if your plan provides a longer post-termination window (extended windows have become common), the option survives — it just converts to NSO treatment when exercised after three months, meaning ordinary income tax on the spread. Read your plan; don't assume.

With NSOs, the terms are set by your option agreement, and many companies give you up to 10 years to exercise. For ISO treatment, the Code allows only two exceptions to the three-month rule: termination due to disability extends the window to 12 months (§422(c)(6)), and if the employee dies, the three-month limit doesn't apply to exercise by the estate or heirs.

Why is this a problem? Because if you leave your company and you want to keep your options, you need to come up with the cash to exercise them within three months. That's not trivial. If you have 10,000 options at a $1 strike price, you need $10,000 in cash, quickly. And remember, you also have to think about the AMT implications. If you exercise a bunch of ISOs right before leaving, you might owe AMT on the spread, even if the stock never becomes valuable.

Many employees are shocked by this rule. They thought they had time to think about it, to see if the company went public or got acquired. Nope. Three months. If you want to hold onto your options, you have to act fast.

NSOs don't have this problem, which is another reason many companies use them for flexibility.

Section 83(b) Elections and Early Exercise

Now we're getting into the really sophisticated territory, and I want to explain this carefully because it interacts with both ISOs and NSOs in important ways.

When your company grants you stock options, the option itself is not valuable for tax purposes—it's just a right to buy stock. But some companies allow "early exercise," meaning you can exercise your options before they've vested. If you do, you own the stock, but the stock is subject to a repurchase right by the company. As the stock vests, the repurchase right lapses.

Here's where Section 83(b) comes in. Section 83(b) of the tax code allows you to make an election that says: "I want to be taxed on the restricted stock I own today, not when it vests." Why would you want this? Because if you're taxed today when the stock is worth very little, but the stock appreciates significantly before it vests, all of that appreciation is capital gain, not ordinary income.

With an NSO that you early exercise, a Section 83(b) election is straightforward. You pay tax today on the spread between strike price and fair market value (usually zero if you exercise while the strike price still equals fair market value). All future appreciation is capital gain.

With an ISO? It's different — and widely misunderstood. For regular tax purposes there is no Section 83(b) election to make on an ISO, because exercising an ISO creates no ordinary income in the first place (§421(a)). The election you file on an early-exercised ISO operates only for AMT purposes: it fixes the AMT adjustment at the exercise-date spread rather than the (likely larger) spread when the shares later vest. See Treas. Reg. §1.422-1(b)(3) and §56(b)(3).

What the election does not do is move the qualifying-disposition clock. The §422 one-year holding period runs from the transfer of the shares at exercise whether or not you file — and the two-year-from-grant period is unaffected by anything you do. File the protective 83(b) within 30 days of an early exercise anyway; the AMT protection alone is worth it, and there is no downside.

This can be useful if your company grants options with a low strike price but you believe the stock will appreciate significantly before vesting. Early exercise plus 83(b) election locks in that low tax basis, and everything else is capital gain.

But it requires careful planning. You need to understand the AMT implications. You need to make sure you actually want to lock in the basis. And you need to make sure your option plan actually permits early exercise.

QSBS and Both ISO and NSO Implications

I've written extensively about Qualified Small Business Stock—QSBS—because the Section 1202 capital gains exclusion is one of the most valuable tax benefits available to startup employees and founders. Here's how it interacts with both ISOs and NSOs.

If you hold QSBS for at least five years and meet all the requirements, you can exclude up to $10 million (or $15 million for stock issued after July 4, 2025) — or 10 times your adjusted basis (the taxpayer’s basis in the stock at original issuance (at least the FMV of any property contributed, per §1202(i)(1))), whichever is greater — in gain when you sell. That's not a deduction, that's an exclusion. You literally don't pay tax on that gain. It's extraordinary.

Both ISOs and NSOs can qualify for QSBS treatment, but the mechanics differ slightly.

With an ISO, your basis is the strike price you paid to exercise the option. If you exercise at $1 per share, your basis is $1 per share. Then you hold it for five years, the company is acquired for $100 per share, and you have a $99 per share gain. If it qualifies as QSBS, you exclude up to $10 million (or $15 million for post-July 4, 2025 stock) of that gain.

With an NSO, your basis is the fair market value at exercise—the strike price you paid plus the spread you already recognized as ordinary income. That's the key point: because you were taxed on the spread at exercise, it's baked into your basis, so you're not "double taxed" on it. The QSBS exclusion then applies to your gain from that exercise-date basis up to the sale price.

Both can qualify for QSBS. The holding period clock starts on the day you exercise the option. The key requirements are: C corporation, aggregate gross assets at issuance of $50 million or less ($75 million for stock issued after July 4, 2025), and the company is engaged in an active trade or business (not investment, real estate, etc.).

Most successful startups meet these requirements. The QSBS benefit is so valuable that if you have a choice between exercising an ISO or NSO, and everything else is equal, the QSBS qualification status should factor into your decision.

Washington State Income Tax: How ESSB 6346 Changes the Calculus

I practice in Washington state, and I have to tell you: Washington just changed the game for ISO and NSO taxation, and almost nobody's paying attention.

In 2026, Washington passed Engrossed Substitute Senate Bill 6346 (ESSB 6346), which imposes a 9.9% income tax on income above $1 million, effective January 1, 2028. (Washington's capital gains tax — a separate 7% excise tax on long-term gains above the annual standard deduction — was enacted earlier, in 2021, as ESSB 5096, and has been in effect since 2022.)

Here's why it matters: Washington doesn't yet have a broad income tax, but since 2022 it has taxed long-term capital gains above the standard deduction. So an employee's qualifying-disposition ISO gain isn't tax-free at the state level—the long-term gain above the deduction already faces Washington's 7% (9.9% over $1 million) capital gains tax. ESSB 6346 adds a separate income tax starting in 2028 — but the two taxes don't stack. The income tax credits the capital gains excise tax paid on the same gain (ESSB 6346 § 205), so from 2028 a qualifying-disposition gain is taxed at roughly 9.9% once, not 19.8%.

Washington's capital gains tax already applies: 7% on long-term gains above a ~$278K standard deduction, rising to 9.9% on the portion above $1 million. On a $5 million long-term gain, after the standard deduction that comes to roughly $438,000 in state tax (7% on the first $1 million of taxable gain, 9.9% above).

For NSOs, the situation is different. The spread at exercise is ordinary income, which will fall under Washington's new income tax once it takes effect in 2028. The capital gain portion is subject to the capital gains tax, which applies to long-term gains only.

This doesn't change the analysis between ISOs and NSOs dramatically—ISOs are still generally better on a federal level—but it does mean that Washington residents should factor state tax into their analysis going forward.

And if you exercise ISOs with a large spread between now and 2028, be aware that when you eventually sell — even after 2028 — the gain will face the Washington tax stack: the capital gains excise tax, plus the income tax with a § 205 credit for the excise tax paid. The state-level answer is the same either way: roughly 9.9% on the taxable portion over $1 million, and the real lever is QSBS, because gain excluded under Section 1202 never enters either tax base.

When Founders Should Grant ISOs Versus NSOs

Now let's talk about what matters to founders: when should you grant ISOs versus NSOs to your team?

Here's my practical framework:

Grant ISOs when: You're granting to employees you want to incentivize for the long term, the company is pre-revenue or early revenue and the strike price is very low, you want to minimize current tax obligations on exercise, and you reasonably believe the company will either go public or be acquired for a significant premium. ISOs are the employee-friendly option, and if your employees understand the rules, they'll appreciate getting them.

Grant NSOs when: You're granting to consultants, advisors, or board members. You're granting to contractors. You're at a later stage and the valuation is high (to stay under the $100,000 annual limit). You want simplicity and don't want to deal with ISO tracking and AMT. You want to get a tax deduction at exercise (more on this below). You want maximum flexibility in timing and terms.

Here's a practical reality: many sophisticated companies grant a mix of both. Early employees (first 10-20 people) get ISOs because the valuation is low and they're core to the team. Later employees and consultants get NSOs. This approach gives you the best of both worlds: you attract early talent with tax-efficient options, and you maintain flexibility for everyone else.

One more thing: founders granting themselves options (unusual, but it happens) should almost always take NSOs — and there's a statutory reason beyond flexibility. Under §422(b)(6) and (c)(5), anyone owning more than 10% of the company's voting power can receive ISOs only if the strike price is at least 110% of fair market value at grant and the option term is capped at five years. For most founders, those conditions kill the ISO's economics before the holding-period complications even come up.

The Company Tax Deduction: An Often-Overlooked Advantage of NSOs

Here's something I don't see discussed often enough: when your company grants ISOs, the company gets no tax deduction when the employee exercises, even though real economic value is being transferred. This is the trade-off for giving the employee favorable tax treatment.

When your company grants NSOs, the company gets a tax deduction equal to the ordinary income recognized by the employee at exercise. If an employee exercises an NSO and recognizes $100,000 in ordinary income, your company deducts $100,000.

For a venture-backed company, this might not matter much until the company is profitable. But for bootstrap companies or companies with other sources of profit, the NSO deduction can be valuable. It's a benefit of granting NSOs that employees often don't understand.

Common Mistakes and How to Avoid Them

The mistakes below are the ones that most often cost people money — usually smart people who simply didn't know the rules.

Mistake #1: Not understanding AMT. An employee exercises a bunch of ISOs with a large spread, doesn't understand they'll owe AMT, and gets a tax bill for hundreds of thousands of dollars. Then their company never goes public and the stock becomes illiquid. The fix: understand the math before exercising. If you're exercising a substantial amount of ISOs, talk to a tax professional about your AMT exposure.

Mistake #2: Missing the $100,000 annual limit. A founder grants options to employees without tracking the annual limit, and options that should have been ISOs become NSOs due to the limit. The fix: if you're granting significant equity, use an option tracking spreadsheet that monitors the aggregate fair market value of ISOs granted per employee per year.

Mistake #3: Forgetting about the three-month post-termination rule for ISOs. An employee leaves the company, thinks they have time to decide what to do, and then realizes they only have three months to exercise. They miss the deadline and lose their options. The fix: have a conversation with departing employees about the exercise deadline. Put it in writing in your option plan and your employee handbook.

Mistake #4: Not holding ISOs long enough for a qualifying disposition. An employee exercises ISOs, the company is acquired or goes public, and they sell immediately. They pay ordinary income tax on the spread instead of capital gains tax because they didn't hold for one year post-exercise. The fix: understand the one-year holding period and plan your exercise and sale timing around it.

Mistake #5: Ignoring Section 83(b) when early exercising. An employee early exercises options without filing an 83(b) election, and the tax treatment is less efficient than it could have been. The fix: if you're early exercising, definitely talk to a tax professional about whether an 83(b) election makes sense.

Strategic Considerations for Growing Companies

As a founder, here's how I think about the strategic decision:

In the earliest days, when you're bringing on co-founders and first employees, you want to be generous with equity and tax-efficient. Grant ISOs. The strike price will be very low, your valuation is uncertain, and early employees deserve the benefit of favorable tax treatment.

As you raise funding and your valuation increases, the ISO math becomes less attractive. That $100,000 annual limit starts to bite. Switching to NSOs gives you more flexibility and avoids the tracking complexity.

By the time you're at Series B or later, most companies have moved entirely to NSOs for new grants, while grandfathering earlier employees' ISOs.

One point that surprises founders: if your company is going to exit, you can often negotiate the exit in a way that's favorable to both ISOs and NSOs. Many acquisition agreements accelerate vesting, which creates a compressed decision for employees holding ISOs with a large spread: employees who are terminated in the post-closing restructuring face the three-month exercise clock and the AMT exposure at the same time. Smart deal teams know this and plan for it — cash-outs, option assumption, and termination timing all change the tax outcome. But it's worth thinking about in your exit planning.

The Bottom Line

ISOs and NSOs are both valuable tools for startup equity compensation, but they serve different purposes and have very different tax consequences.

ISOs are better for employees when the company is early-stage, the strike price is low, and there's a reasonable path to a significant exit. The tax deferral and potential capital gains treatment are genuinely valuable. But the AMT trap, the three-month post-termination rule, and the $100,000 annual limit create complications that need to be managed carefully.

NSOs are simpler, more flexible, and essential for non-employee grantees. They don't have the ISO restrictions, they can be granted to consultants and advisors, and they give the company a tax deduction. The downside is that employees pay ordinary income tax immediately on the spread, which can be a significant burden if the strike price is very low relative to the company's valuation.

The right choice depends on your specific situation: the stage of your company, the valuation, who you're granting to, and your tax circumstances. There's no universal answer.

But here's what I know from decades of advising startups: founders and employees who understand these rules make better decisions. They exercise at the right time, they hold for the right length of time, they plan for the tax consequences, and they actually benefit from the equity they've been granted instead of being blindsided by unexpected tax bills.

That's what this guide is really about. Understanding the rules so you can use them to your advantage, instead of having them blindside you. The difference between people who understand equity compensation and people who don't is measured in six figures.

Related Posts

- Section 83(b) Elections: What Startup Founders and Employees Need to Know

- The Complete 83(b) Election Guide

- Stock Option Exercise Timing and Washington Income Tax

- Qualified Small Business Stock (QSBS): What Founders, Investors, Contractors, and Employees Need to Know

- 409A Valuations: What Every Startup Needs to Know

- SAFE Agreements: What Every Startup Founder Needs to Know

Ready to Build on a Solid Legal Foundation?

If you're a founder working on equity compensation strategy, or an employee trying to understand your options, I'd be happy to talk through your specific situation. Stock option decisions can have real financial consequences, and getting them right matters.

Schedule a free introductory call to discuss your startup's equity and tax strategy. I work with founders and early employees across Washington state and beyond.

Related Reading

This post is for educational purposes only and is not legal or tax advice. Consult a qualified attorney about your specific situation.